Objections to the on-site tax audit report: procedure for filing and deadlines for consideration. Objections to the inspection report: recommendations for drafting

Each company has the right to file an objection to the act tax audit, if you do not agree with the inspectors. In the article - general rules and a sample objection to 6-NDFL.

When to file an objection

Objections can be filed within a month from the date of receipt of the desk or field inspection report in case of disagreement with the facts stated in the report:

- tax audit (clause 6 of article 100 of the Tax Code of the Russian Federation);

- on the discovery of facts indicating tax offenses (clause 5 of Article 101.4 of the Tax Code of the Russian Federation).

The period is counted from the day following the receipt of the inspection report (clause 2 of article 6.1 of the Tax Code of the Russian Federation). The deadline for submitting objections expires on the corresponding date of the month following the month of receipt of the desk inspection report (Clause 5, Article 6.1 of the Tax Code of the Russian Federation).

Example:

“The company received a tax audit report on June 11, 2018. This means that objections must be submitted no later than July 11, 2018. If the end of the period falls on a month in which there is no corresponding date, then the last day on which objections can be submitted expires on the last day of this month (Clause 5, Article 6.1 of the Tax Code of the Russian Federation).”

The company is interested in submitting objections in a timely manner. If you are late, review of materials checks will pass without objections. This means that the inspectors will make decisions without taking into account the company’s opinion on controversial issues.

How to make objections

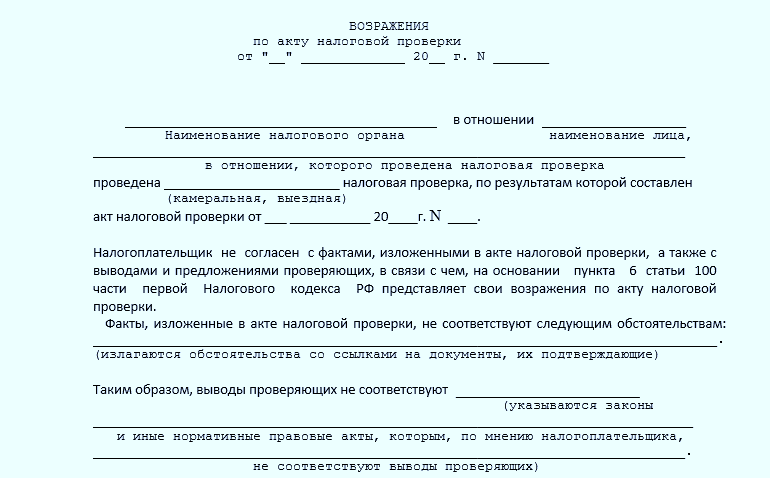

There is no approved form of objection to a tax audit report. The Tax Code of the Russian Federation does not contain requirements for the format and content of such a letter. Therefore, draw up objections in any form in two copies. Give one to the inspectorate, keep the second in the organization.

First of all, list in your objections:

- name of the inspectorate to which objections are submitted;

- company name (last name, first name and patronymic individual entrepreneur);

- TIN and checkpoint (if any);

- registration address, as in constituent documents(address of permanent registration of the entrepreneur);

- date of submission of objections;

- names of taxes or declarations (calculations) in respect of which the audit was carried out, indicating the period;

- start and end dates of the audit.

Then you need to cite specific points of the act with which the company does not agree. Preferably in order. Written objections can be submitted to the act as a whole or to its individual provisions.

It is important to list only those claims that are directly related to the conclusions and proposals of the tax inspectorate formulated in the audit report. Even if there were formal violations of the inspection procedure or the act itself contains any shortcomings, there is no need to mention them in objections.

Oleg Khoroshy answers,

Head of the Corporate Income Tax Department of the Department of Tax and Customs Policy of the Ministry of Finance of Russia

“Submit objections to the tax audit report in writing. You can attach documents that confirm the validity of the objections. In addition, supporting documents can be submitted to tax office and separately from objections within a pre-agreed period. Send objections and documents to the inspectorate whose employees conducted the inspection. This is stated in paragraph 6 of Article 100 of the Tax Code.”

Therefore, if the company’s comments relate only to the inspection procedure, and not to the erroneous position of the inspectors, then there is no need to file objections at all. After all, they are unlikely to influence the inspectors’ decision. Such claims can be raised later when appealing the decision.

The company's arguments for each episode must be convincing. Therefore, your position must be stated as clearly as possible and, if possible, justified by referring to legal norms. Moreover, in your arguments you can only refer to the norms that were in force during the period when the audit was carried out. Additionally, you can provide links to official explanations of the Russian Ministry of Finance and the Tax Service.

- Which letters from the Ministry of Finance should be cited in objections to the inspection report:

- It is safer to be guided by those letters from the Ministry of Finance that are addressed to your company. A reliable option would be the explanations posted on the official website of the Federal Tax Service of Russia (nalog.ru) for mandatory application. Of course, in the Tax Code of the Russian Federation there is a norm obliging tax specialists to be guided by written explanations of the Ministry of Finance on the application of tax legislation (subclause 5, clause 1, article 32 of the Tax Code of the Russian Federation). However, the ministry itself has repeated more than once: this norm Tax Code The Russian Federation does not require tax authorities to follow absolutely all explanations. The fact that clarification is mandatory must be stated in the letter itself. But letters addressed to other companies can also play a role as an additional argument.

You can also select examples from judicial practice: decisions of the Supreme Court, decisions of arbitration courts. Copies of the documents referred to must be attached to the objections.

Objections to the act can be signed by either the head of the company or another employee by proxy. For example, chief accountant.

Objection to the report of a desk tax audit under 6-NDFL

Tax officials send 6-NDFL inspection reports to companies. In them, tax authorities report, for example, that a company was late with the payment of personal income tax, and cite periods when the organization transferred tax at the wrong time. For this, a fine is imposed - 20 percent of the late tax (Article 123 of the Tax Code of the Russian Federation).

Sometimes the sample of personal income tax debtors mistakenly includes companies that have not violated tax payment deadlines. The Federal Tax Service program does not always correctly compare the terms from section 2 of the calculation of 6-NDFL and payment bills. If you are sure that personal income tax was paid on time, you need to inform the tax authorities about this.

Prepare written objections to the desk tax audit report under 6-NDFL in free form. In it, tell us why you do not agree with the fine from the act. To do this, you have a month after the date when you received the act in person, by mail or through a special operator (clause 6 of Article 100 of the Tax Code of the Russian Federation).

Sample objection to a tax audit report under 6-NDFL

To make objections to tax authorities, use our sample below. Download ready-made example document can be found at the link below. It's free.

Objections to the tax audit report for calculation of 6-NDFL (sample)

How to register applications

The company has the right to attach to the objections any documents confirming the validity of the objections. These papers can be submitted to the inspection separately - within a pre-agreed period (clause 6 of Article 100 of the Tax Code of the Russian Federation).

A copy of each document must be certified separately, and not the file as a whole (letter of the Ministry of Finance of Russia dated October 29, 2014 No. 03-02-07/1/54849). This still applies to absolutely all documents - both single-page and multi-page.

One Page Documents. It is safer to certify each one-page document separately. If the company does not have time to prepare copies, you can ask to extend the deadline for their submission.

Another riskier option is to form a binder from copies of documents and make one certification inscription on it. In such a situation, inspectors may demand that the company pay a fine of 200 rubles. for each incorrectly certified document (clause 1 of Article 126 of the Tax Code of the Russian Federation).

But this fine can be canceled in court, since there is no liability for incorrect certification of documents in the law (resolution of the Federal Antimonopoly Service of the Central District of November 1, 2013 in case No. A54-8663/2012).

Multi-page documents. The company has the right to certify a copy of a document consisting of several pages with one inscription. It is not necessary to certify each sheet of the copy (letter of the Ministry of Finance of Russia dated August 7, 2014 No. 03-02-RZ/39142, Federal Tax Service of Russia dated September 13, 2012 No. AS-4-2/15309). For example, a copy of a multi-page agreement can be created in the form of a binder. And make one general certification inscription on it. But in this case, all sheets of a multi-page document must be sewn together with thread and numbered.

A certification record can be made in two ways: back side the last sheet in the bundle or on a separate sheet.

On the sheet they make a note “correct” or “copy is correct”, put the date, position of the manager or other employee who certified the copy, as well as his signature with a transcript (clause 3.26 of the State Standard “Unified Documentation Systems”, approved by the resolution of the State Standard of Russia dated 3 March 2003 No. 65-st).

Where and how to submit objections to a tax audit report

Written objections must be sent to the inspection that conducted the inspection and drew up the report (clause 6 of Article 100 of the Tax Code of the Russian Federation). Objections can be submitted personally to the inspection office or document acceptance window by the head of the company or its representative on the basis of a power of attorney (Articles 27, 29 of the Tax Code of the Russian Federation).

You can also send objections by mail. In this case, the monthly period for filing objections must be counted from the seventh day from the date of sending the registered letter. The fact is that the date of delivery of the act sent by registered mail, it is not the day of its actual receipt that is considered, but the sixth day from the moment it was sent by mail (Clause 5 of Article 100 of the Tax Code of the Russian Federation).

What are the consequences of filing an objection?

Objections can both help the company - reduce or cancel the fine, and complicate the process of processing the inspection results. Therefore, it is important to anticipate possible consequences in a timely manner.

Additional activities after filing objections

When filing objections, it is important to take into account that this may provoke additional tax control measures (clause 6 of Article 101 of the Tax Code of the Russian Federation). In this case, it becomes necessary to extend the time for reviewing the inspection materials. The period for carrying out additional activities should not exceed the total period for reviewing inspection materials, taking into account its extension - 10 working days and another month.

Accordingly, a decision based on the results of the inspection will be made taking into account new information obtained during additional activities.

Additional activities may include:

- requesting documents from the company or its counterparties;

- interrogation of a witness;

- conducting an examination.

Before the inspectors take out final decision, the company has the right to familiarize itself with all inspection materials, including the results additional materials(Clause 2 of Article 101 of the Tax Code of the Russian Federation).

A specific deadline has been set for this: no later than two days before the consideration. The company is required to submit an application to familiarize itself with the materials. If such a statement is not submitted in a timely manner, inspectors may not take the initiative.

Of course, the Federal Tax Service of Russia, in its explanations, advises its subordinates to familiarize the company with the materials of additional events in any case. After all, otherwise the taxpayer will be able to cancel the decision made based on the results of the audit on formal grounds.

At the same time, no special deadline has been established for the company to prepare its arguments (Article 101 of the Tax Code of the Russian Federation). Tax officials can agree with the company on the time it will take to file objections. And then, after reviewing the inspection materials, the inspector will make a note in the protocol that the organization had no objections regarding this time (letter dated August 22, 2014 No. SA-4-7/16692 - excerpts from the document, paragraph 38 Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 No. 57).

This is beneficial for the company. Indeed, sometimes inspectors do not even offer companies to familiarize themselves with the materials of additional events. And sometimes they only give a couple of hours to study several hundred pages, effectively depriving the company of the opportunity to study all the details and present objections.

The clarification of the Federal Tax Service of Russia, firstly, motivates local inspectors to always transfer the materials of both the inspection and the additional event to the company for review. Otherwise, the decision they make may be reversed.

Secondly, the company has the opportunity to agree on the time it will need to prepare objections. This means that you can carefully study all the inspector’s findings and try to fight off some of the additional charges and fines.

The decision to refuse to prosecute must indicate the circumstances on the basis of which it was made. At the same time, it may reflect the amounts of arrears identified during the audit and the corresponding amounts of penalties. This follows from the provisions of paragraph 2 of paragraph 8 of Article 101 of the Tax Code of the Russian Federation.

In addition, both types of final audit decisions must reflect the following data:

- the period for appealing the decision;

- procedure for appealing a decision to a higher authority tax authority;

- name and address of the tax authority that is authorized to consider cases of appealing the decision;

- other information necessary, in the opinion of the head of the inspection (his deputy).

This is stated in paragraph 3 of paragraph 8 of Article 101 of the Tax Code of the Russian Federation.

If during a tax audit, inspectors discover an amount of over-refunded tax, then in the final decisions they will recognize it as arrears. The date of occurrence of this arrears will be the day when the organization received the money (upon return) or the day when the inspectorate decided to offset the tax.

This is stated in paragraph 4 of paragraph 8 of Article 101 of the Tax Code of the Russian Federation.

Within five working days after the decision is made based on the results of the inspection, it must be handed over to the organization (paragraph 1, paragraph 9, article 101, paragraph 6, article 6.1 of the Tax Code of the Russian Federation). The countdown of the period begins from the next day after the decision is signed (clause 2 of article 6.1 of the Tax Code of the Russian Federation). Let's give an example.

Example:

“The decision on the inspection was made on July 9, 2018 (Friday). The company must receive it no later than July 16, 2017.”

As a general rule, the inspection decision comes into force one month from the date it is delivered to the organization (clause 9 of Article 101 of the Tax Code of the Russian Federation). But if during this month the organization appeals it on appeal, then the date of entry into force will depend on what decision the higher tax authority makes.

If the decision of the tax inspectorate is not canceled, it will come into force from the date of its approval by a higher authority.

If the decision of the tax inspectorate is canceled (in whole or in part), it will come into force (taking into account the changes made) from the date of the corresponding decision of a higher authority.

If the appeal is rejected, the decision of the tax inspectorate will come into force from the date of the decision of the higher authority, but not earlier than the month period allotted for filing the appeal has expired.

This procedure is established by Article 101.2 of the Tax Code of the Russian Federation.

After the decision on the inspection comes into force, the inspection, within 20 working days, will send to the organization a demand for payment of taxes, penalties and fines that were additionally accrued based on the results of the inspection (clause 6 of article 6.1, clause 2 of article 70 of the Tax Code RF).

The organization is obliged to fulfill this requirement within eight working days after its receipt, unless a longer period is established in the requirement itself (paragraph 4, paragraph 4, article 69, paragraph 6, article 6.1 of the Tax Code of the Russian Federation).

An objection to an act of desk and field inspection is a procedure in which disagreement is expressed with the decision of tax or other regulatory authorities and funds (FSS, Pension Fund).

Procedure

The sequence of actions of a taxpayer who has received the results of a tax audit is given below.

- Issuance of an inspection report.

- Analytical study of the received document for legality by the manager, accountant and lawyer.

- Decision to file an objection.

- It is sent to the tax authorities.

To prepare an objection, the taxpayer has 10 days for a desk audit or 2 months for an on-site audit. Perhaps this is the difference of this document regarding the type of check.

Depending on who carried out the inspection, the deadline for submitting a document of disagreement may vary (Federal Tax Service, Social Insurance Fund or Pension Fund), so in each case it is necessary to clarify them. The document is drawn up if the subject entrepreneurial activity I don't agree:

- with an inspection report (clause 6 of Article 100 of the Tax Code of the Russian Federation);

- with facts tax violations discovered during the inspection (clause 5 of Article 101).

The ten-day or two-month period is counted from the next day after receipt of the act (clause 2 of article 6.1 of the Tax Code of the Russian Federation).

Do not be late in filing an objection to the desk tax audit report, then you will have more chances to defend your case

How to determine the deadline for filing an objection?

For example, an enterprise was issued an act on April 10, 2017. In this case, the last day for filing an objection is April 20, 2017 for office and June 10, 2017 for offsite.

There are cases when the deadline falls on a date that does not exist in that month, then last day to submit an objection is the last calendar day of this month.

For example, the tax inspectorate presented the company with an on-site inspection report on July 31, 2016. This means that the last day for an objection will be September 30, 2016.

Previously, the requirements for meeting deadlines were more stringent, now you can object later, but it is still recommended to meet the deadlines.

If, nevertheless, the entrepreneur is delayed, objections can be prepared at the time of consideration of the inspection materials, where a representative of the party being inspected is invited. It is at this meeting that objections should be accepted and taken into account during the discussion.

Drawing up a document of disagreement with the decision of the tax service

Taking into account the fact that this document has features inherent to a single business entity, there is no unified form. The objection is drawn up in free form, but there are General requirements to its content.

How to write about disagreement with the results of an inspection

The document must contain all of the following information.

- The name of the tax service to which these objections will be submitted.

- Full name of the enterprise or full name. I. O. IP.

- If available, indicate the Taxpayer Identification Number (TIN) and KPP.

- Legal address of the company, IP registration address.

- Day, month and year of the submitted document.

- List the taxes or other calculations that were the subject of the audit, indicating the period.

- The exact start and end dates of the check.

- Information about inspection inspectors.

A standard letter structure is provided as a guide.

- An introductory part consisting of 2-3 paragraphs.

- Descriptive, it contains the main text.

- Resolution.

- Conclusions and requests.

The text of the objections clearly identifies the points with which the taxpayer does not agree. It is advisable to list them in the same sequence as in the act. Depending on the scope of objections, they can be filed either against the act as a whole or on individual points. Objections should not mention misunderstandings during the inspection; the main thing is to state specific claims supported by facts.

It is necessary to understand the nature of the disagreement with the opinion of the tax authorities, because if we are talking only about violations of the audit procedure itself, objections will not be filed. Similar claims can be made when appealing a decision.

For each point, it is necessary to provide compelling arguments confirming the taxpayer’s position. Each justification must have a link to a specific article of the law.

When drawing up objections to the inspection report, it is necessary to refer to the relevant articles of the law

In addition to the basic legislation in the field of tax policy, there are letters from the Ministry of Finance, in particular, addressed to this enterprise. If you refer to them, the objection will be more convincing. It would also be advisable to refer to the explanations offered by the Federal Tax Service on the official website.

It would be useful to turn to colleagues who have already found themselves in a similar situation. In addition, they have letters from the Ministry of Finance and explanations from the Federal Tax Service, which are necessary when drawing up an objection.

You can use examples of court decisions, make copies of documents from the Supreme and Arbitration Courts.

Objections are signed either by the manager or by an authorized representative.

To prove its case, the company can draw up an annex to the main document. It should be sent to the inspection body separately from the objection within the specified period (clause 6 of Article 100 of the Tax Code of the Russian Federation).

How to prepare your documents

Each document must be certified separately with a signature and seal. There is another way - all copies are submitted in the form of a binder and certified by one certification. However, this form does not always suit tax inspectors, who can find fault with the fact that documents are certified with violations and even impose a fine of 200 rubles for this. for each incorrectly executed document.

Although, as practice shows, such actions on the part of tax authorities are recognized by the court as unlawful and fines are cancelled.

Multi-page documents must be numbered, stitched and certified: “correct” or “copy is correct”, date, position, full name and signature with a transcript of the person who signed the document.

Participation in the consideration of the desk inspection report

After receiving notice in writing or by telephone, it is advisable to attend the meeting, especially if the entrepreneur is confident in the legality of the objections raised.

To participate in the meeting you must have the following documents with you:

- identification;

- power of attorney, if not the manager, but his representative will be present;

- a copy of the main document about disagreement with the results of the “camera chamber”;

- checking act;

- Application.

It is also necessary to prepare theoretically, think through a logical and reasoned presentation, give real examples, and focus on the explanations of the Ministry of Finance, the Federal Tax Service, the Pension Fund and the Social Insurance Fund.

You can use a moment that can play in favor of the person being tested. For example, if he is not sure that he can prove that he is right, it is not necessary to appear at the meeting. However, you can then submit an application to higher authorities or the court to appeal the decision due to a violation of the review procedure, which occurred in the absence of the taxpayer.

Please note: before a decision is made on the complaint ( appeal) you have the right to withdraw it in whole or in part. To do this, you must send a written application to the tax authority. In this case, you lose the right to re-file a complaint on the same grounds.

clause 7 art. 138 Tax Code of the Russian Federation

Preparation of written objections based on the results of VAT and income tax audits

Objections to the VAT audit report boil down to a request to assign additional control procedures

In the example above, the taxpayer protests against the results of the VAT desk audit report, describes the facts presented in the document as unlawful and asks to schedule additional verification activities.

Correct objection to the income tax audit report: the taxpayer justifies the legality of his actions

In an objection to the inspection report, one should not only write down the violations committed during the inspection, but also justify the correctness of determining the tax base, the application of deductions or the calculation of tax amounts.

Disagreement with the opinion of the inspectors must be supported by references to the relevant regulatory documents

How and where to send an objection?

The prepared document is sent in writing to the address of the territorial tax inspectorate that carried out the audit (clause 6 of Article 100 of the Tax Code of the Russian Federation), or transmitted directly to the office. This can be done by a leader or a trusted person (vv. 27, 29). It is advisable to prepare two copies, one for the tax office, the other with a mark of acceptance remains with the applicant of objections.

If it is not possible to submit the document in person, it can be sent by registered mail by regular mail. Here it is very important to pay attention to the timing when the date of delivery is considered the sixth day from the day of mailing (clause 5 of Article 100 of the Tax Code of the Russian Federation).

Letter consideration time

The objection is considered by the head or his deputy of the tax inspectorate conducting the audit. The deadline for completing the review is determined by the tenth day after the deadline for submitting an objection, and not from the moment it is received from the taxpayer being audited. Based on clause 1 of Article 101 of the Tax Code of the Russian Federation, this period can be extended to 1 month.

After consideration, an appropriate decision is made. Depending on the real state of affairs, tax authorities can:

- hold one or more tax inspectors accountable for violating tax laws;

- prepare a refusal to prosecute due to non-recognition of the offense committed tax officers(Clause 7 of Article 101 of the Tax Code of the Russian Federation).

What to do after submitting an objection?

The head of the company or individual entrepreneur will have to wait for the result within the allotted time to consider the objection. Upon expiration of the period, the taxpayer receives a notification about the decision taken. If this does not happen, you should contact the tax service and find out the reason. When it turns out that the tax authorities are clearly ignoring the consideration of the document of disagreement with the audit report, you should not dwell on this. For further actions, there are higher supervisory and judicial authorities.

What to do if the Federal Tax Service refuses to accept an objection

Some taxpayers are faced with the fact that inspectorate employees are not going to accept objections within the acceptable time frame. This fact is a direct violation on the part of the regulatory authorities. In such a situation, it is necessary to contact the appropriate higher authorities or the court.

Lawyers recommend using such measures only in cases where the entrepreneur is completely confident that he is right. It should be remembered that the trial procedure is quite lengthy and requires financial costs. However, you should not refuse it if the taxpayer has enough legal grounds, supported by documents, which guarantees that a decision will be made in his favor.

As a rule, any tax audit ends with the identification of certain violations. However, such actions of regulatory authorities are not always objective; sometimes elementary mathematical errors in calculations or obvious violations of tax legislation occur. To achieve justice, the taxpayer can use a convenient tool, which is an objection to the tax audit report. It is enough to fill it out in accordance with the requirements of the law, explain your position and submit the document to the tax office in a timely manner.

Objections to the desk inspection report - sampleYou can completely compose them yourself. To do this, it is enough to take into account several factors, which will be discussed in this article.

When should you file objections to a desk inspection report?

If a taxpayer has doubts about the legality of the tax authority’s position based on the results of a desk audit, he should file an objection. Moreover, the document must be drawn up in writing, because:

- this is how you demonstrate the seriousness of your intentions;

- the inspection or department of the Federal Tax Service will not consider it in any other form;

- it may be needed in court.

Naturally, you should select very convincing arguments that can sway the opinion of a higher authority or court in your direction.

At the same time, the taxpayer must keep in mind that filing objections is fraught with additional checks - the tax inspectorate, according to clause 6 of Art. 101 of the Tax Code of the Russian Federation, is obliged to respond to the signal. A similar situation is reflected in several court decisions, in particular in decisions of the FAS East Siberian District dated July 15, 2009 No. A58-4792/08, FAS Moscow District dated September 9, 2009 No. KA-A40/8644-09 and the FAS Northwestern District dated 06/01/2009 No. A56-26710/2008.

It may happen that tax inspectors, during an additional audit, will find even more serious violations. Therefore, when filing objections to the cameral’s act, you should once again carefully make sure that you are right and all the documents are in order.

You will learn about the timing of the desk audit from the article .

In what situations should you not file objections to a desk inspection report?

Formal violations committed by inspectors should not be noted in objections, such as: start and end dates of the event, procedural framework, inaccuracies in the preparation of the protocol. It's better to focus on the essence of the act.

If the taxpayer has comments only on formal reasons, then it is better not to file objections. They can be left to appeal decisions made based on the results of the desk audit. In court, in this way it will be possible to try to discredit the act. If you do this earlier, the tax authority will eliminate the shortcomings and deprive the taxpayer of arguments.

Read about what you need to be prepared for when checking your income tax return. .

Objections to a desk tax audit report: sample

In the Tax Code and others legislative acts There are no separate requirements for filing objections to a desk tax audit report. Therefore, the taxpayer can present arguments in any form.

Here is a sample objection to a desk audit report.

Example

The tax authority, represented by senior tax inspector I. I. Zaitseva, conducted a desk audit of the VAT return filed by Omega LLC for the 3rd quarter of 2017. In the act dated January 18, 2018 No. 18-4/23, Zaitseva proposes to charge additional VAT for the 3rd quarter of 2017 and charge penalties on the tax. Claims from the tax inspectorate arose under the supply agreement with Gerkon LLC.

The manager, accountant and lawyer of the company familiarized themselves with the act and believed that they would find compelling arguments to convince the tax authorities to correct the amount of the claim. As a result, a document was drawn up - an objection to the desk inspection report.

To the head

Inspectorate of the Federal Tax Service of Russia No. 23 for St. Petersburg

196158, St. Petersburg,

st. Pulkovskaya, 12, letter A

from Omega LLC

TIN 7801378904, checkpoint 771801991

196158, St. Petersburg,

Moskovsky Ave., 136

Objections

Omega LLC for a desk tax audit report

dated January 18, 2018 No. 18-4/23

Inspectorate of the Federal Tax Service of Russia No. 23 for St. Petersburg, represented by senior state tax inspector I. I. Zaitseva, conducted a desk audit tax return for VAT of Omega LLC for the 3rd quarter of 2017.

In the act No. 18-4/23 dated January 18, 2018, drawn up by inspector I. I. Zaitseva, our company was asked to pay the arrears of value added tax in the amount of 172,800 rubles. and penalties accrued in this regard in the amount of RUB 4,354. In addition, it is proposed to bring the company to tax liability for the violation.

We believe that the conclusions of inspector I. I. Zaitseva are unfounded for the following reasons:

Clause 2.4 of the contested act states that the deduction amount is 172,800 rubles. declared incorrectly, since our company did not receive the goods from Gerkon LLC (TIN 77876091011 / KPP 778609001). For this reason, the sale of these products did not take place.

In support of this, the inspector referred to the fact that our company had not paid for the goods, and the counterparty had all the signs of a fly-by-night company registered to extract unlawful tax benefits.

However, Omega LLC is able to confirm with documents the reality and legality of the transaction. Based on the documents attached to the objections, you can verify that goods in the amount of 48 tons were received, entered into the warehouse, and then sold to other contractors. The following documents are attached:

- copyaccounts- texturesfrom№ 184 28.09.2017, exhibitedOOO« Reed switch» Vaddressoursocietyongeneralamount 1 132 800 rub., VvolumenumberVAT 172 800 rub., behindfertilizerscompanies« Syngenta» Vvolume 48 tons;

- copycommodityoverheadfrom 28.09.2017 № 184/14, dischargedonamount 1 132 800 rub., VvolumenumberVAT 172 800 rub., behindfertilizerscompanies« Syngenta» Vvolume 48 tons;

- copyagreementsuppliesgoodsVvolume 56 tonsfrom 15.09.2017 № 49, prisonerbetweenOOO« Omega» AndOOO« Reed switch» ongeneralamount 1 321 600 rub., AndadditionallyprisonerTospecifiedagreementagreementsOdecreasepartiesbefore 48 tons.

- copyaccounts- texturesfrom 28.11.2017 № 337, whichexhibitedVaddressOOO« Agricultural center» onamount 1 359 360 rub., VvolumenumberVAT 207 360 rub.;

- copycommodityoverheadfrom 28.11.2017 № 337, whichexhibitedVaddressOOO« Agricultural center» onamount 1 359 360 rub., VvolumenumberVAT 207 360 rub.;

- copytaxdeclarationByVATbehind 4- thquarter 2017 of the year;

- copiespaymentinstructionsOtransfermonetaryfundsOOO« Reed switch» from 14.11.2017 № 532 Andfrom 28.12.2017 № 664;

- copiesrequestsOtaxdetailsOOO« Reed switch» AndanswersBythisrequests, testifying, WhatthiscompanyNotiscompany- one-day.

In addition, we clarify that the delivered products were indeed not paid for in the 3rd quarter of 2017, since in clause 4.2 of the supply agreement the payment period is specified until December 31, 2017.

Director of Omega LLC Pavlov Pavlov E.I.

Results

A desk tax audit report is issued by tax authorities only if violations were discovered during control of the declaration. You can send your objections to the inspection in writing if you can substantiate the fallacy of the conclusions set out in the inspection report.

If there are not enough arguments, it is dangerous to file objections - they may provoke additional tax control measures.

If a taxpayer has doubts about the legality of the actions or demands of the tax inspector who conducted the “camera audit,” he has the right to file an objection to the desk tax audit report, a sample of which is presented below. How to formulate it correctly and in what case should it not be submitted? We will try to give a detailed answer to each question.

Reasons for filing an objection

Tax inspectors, having received the taxpayer's declaration and other documents on income/expenses, conduct a desk audit of these business papers. In the event that any information requires clarification or clarification, the payer is notified accordingly. Within the time limits established by law, he is obliged to provide all Required documents, certificates, etc. Identified violations become the basis for drawing up an inspection report, which is sent to the person being inspected.

If an entrepreneur (the head of an organization) decides that his rights were violated during the audit, he has the right to file an objection to the desk tax audit report.

Experts conditionally divide the reasons for its compilation into two categories:

- procedural violations (the rules for holding a “camera room” were violated);

- violations of substantive law (the inspector misinterpreted some papers and did not take into account all the documents that the payer provided).

There are violations that are not considered serious, and an attempt to point them out may turn against the taxpayer. You should not focus on the following shortcomings of the inspector:

- timing of the “camera room” (beginning and completion);

- minor inaccuracies in the preparation of the act;

- frivolous violations of regulations.

The document must be submitted to the tax office in person or sent by mail. In the latter case, it is advisable to send it by registered mail with notification. Alternatively, you can use the Internet. However, this option is only suitable for those who have a digital signature (officially registered).

Features of compilation

Before drawing up an objection, it is recommended to make sure that violations by inspectors actually took place, and that there are no pitfalls or errors in the entrepreneur’s activities. Otherwise, another (repeated) inspection may reveal serious violations in the activities of the entrepreneur himself.

The document must be submitted on paper because:

- only in this form will it be accepted by a higher tax authority;

- it may be needed when going to court.

All wording must be clear, and the argumentation must be 100% complete. Otherwise, legally savvy government officials. employees will be able to quickly “unravel” an incorrectly drafted taxpayer accusation.

Sample document

To date, there is no clearly defined form of objection. Even the official website of the Federal Tax Service provides an approximate example. However, the logic and norms of office work suggest what and how should be indicated:

- at the beginning of the document (upper right corner) – information about the addressee (name of the tax organization, name, surname and position of the tax inspector who conducted the desk audit);

- further – information about the sender (taxpayer);

- then - the document number and the date of its preparation.

In the main part of the document you should write its name (“Objection to the act...”) and provide your evidence of the identified violations. It is recommended to refer to the articles of the Tax Code, Letters of the Ministry of Finance and other regulations.

In the final part, the payer needs to summarize and indicate his request (requirements). If any documents are attached to the objection, a list of them should be provided in the “Appendix” section. The document must be signed official(head of the company). It is necessary to indicate his position, last name, first name and date.

It is not specified at the legislative level how an objection to the “camera chamber” act should be formalized. This means that you can fill out a ready-made form by hand or print it on a computer using a word processor and then print it on a printer using a regular A4 sheet or company letterhead. It is also not necessary to put a company seal. This rule was canceled in 2016.

The objection is drawn up in two copies. The taxpayer keeps one for himself after the tax inspector endorses him. Another copy is given to the tax office.

State employees are required to notify the taxpayer of the date, time and place of his objections. He can be present and supplement his claims with new arguments or petition for a reduction in the fine, since there are mitigating circumstances (in this case, the amount should be halved). However, his presence is not necessary; it will not worsen the situation.

So, an objection to the desk audit report is a document drawn up by the taxpayer. The reason for compilation is the actions of the inspector who conducted the inspection, which, in the opinion of the payer, violated legislative norms and the rights of the person being inspected. There are no strict requirements for its design, but it is advisable to draw it up if there are compelling reasons.

How to make objections to? Follow a few rules. So, your arguments should be as clear and intelligible as possible. Avoid long and confusing wording.

Present your arguments in the same sequence, in the same paragraphs and subparagraphs that the inspection used. This will be more convenient for everyone. In this case, it is better to preface the arguments brief description positions of the Federal Tax Service.

...

According to paragraphs 2.1.1, 2.1.2, 3.1.1, 3.1.2 of the Inspection Report

The inspectors found that, in violation of subsection. 23 clause 1, clause 3 art. 264 of the Tax Code of the Russian Federation, the organization included in other expenses expenses in the amount of XXX XXX rubles. for employee training consulting company, which does not have a license for educational activities.

We do not agree with this conclusion for the following reasons.

...

Links to legislation

All links are to legislation, letters from the Ministry of Finance, the Federal Tax Service and the Federal Tax Service, as well as to judicial practice- it is better to indicate in parentheses after the arguments. Remember that you need to refer to the norms of the Tax Code and other laws in the wording that was in force during the period under review, and not at the time when you are drawing up objections.

Arbitrage practice

Referring to judicial practice, select the most recent decisions and present them in the following order:

Objections to the tax audit report are made in any form. A sample objection can be found at Federal Tax Service website .

1) acts of the Constitutional, Supreme Arbitration or Supreme Courts(resolutions of the Plenum, Presidium, newsletters, definitions);

2) regulations arbitration court your county;

3) acts of lower courts in your region;

4) acts of courts of other regions.

At the same time, choose those solutions in which the circumstances of the dispute are as similar as possible to your situation. If in your objections you write that your position is supported by extensive judicial practice, then give at least three or four solutions.

In turn, if the tax authorities in the act refer to judicial practice, then you need to try to refute each such reference, for example, on the following grounds:

- the legislation has already changed;

- the given decision does not relate to the subject of the dispute;

- there were other factual circumstances in the case;

- later decisions take a different position.

Extenuating circumstances

In the final part of your objections, do not forget to ask the Federal Tax Service to take into account clause 1 art. 112 Tax Code of the Russian Federation, if in your case they exist. Indeed, if there is at least one such circumstance, the amount of the tax penalty should be reduced least twice clause 3 art. 114 Tax Code of the Russian Federation.

Here are examples of circumstances that absolutely everyone can refer to:

- bringing to tax liability for the first time;

- lack of intent to commit a violation;

- repentance and admission of guilt;

- conscientiousness of the taxpayer, which consists in timely payment of all taxes and submission of reports;

- heavy financial condition, documented, in particular the presence of a large amount of debt.

In your objections, you can also ask to take into account undeclared losses from previous years, the size and presence of which the Federal Tax Service did not dispute. Some courts believe that inspectors cannot refuse the taxpayer this Resolution of the FAS ZSO dated June 25, 2014 No. A27-14009/2013; FAS PO dated 02/04/2014 No. A49-2641/2013. But there are those who have a different opinion see, for example, Resolution of the Federal Antimonopoly Service dated December 3, 2015 No. F09-8175/15.

Attachments to objections to the tax audit report

Attach to your objections copies of primary and other documents proving your case in the controversial episodes. Note that this is not necessary, but it is advisable. Copies must be certified by the manager (IP) or his representative by proxy. Please provide a list of attachments at the end of your objections.

If you cannot attach certain documents to the objections at the time of their submission, then you have the right to submit them later within the period agreed with the Federal Tax Service clause 6 art. 100 Tax Code of the Russian Federation.

Signing objections

Objections must be signed by the head of the organization (entrepreneur) or a person authorized by a power of attorney. In the latter case, a copy of it must be attached to the objections. You can also put a stamp on objections if the company uses it.

Filing objections to the tax audit report to the tax office

There are two ways to submit objections:

- by submitting two copies of the text to the office of the Federal Tax Service or to the document acceptance window. This can be done by the manager himself or his authorized representative. The inspector will accept one copy with attachments, and mark acceptance on the second;

- by mail with a valuable letter with a description of the contents and a notification of delivery. In this case, try to send the letter in advance so that it has time to arrive at the Federal Tax Service before the date of consideration of the inspection materials.

If it so happens that you file objections on the last day of the allotted month, then at least try to bring them directly to the inspectorate. And warn the Federal Tax Service that the objections are directed at her. After all, if you send them by mail, they may not have time to arrive at the inspection by the day the materials are reviewed. And then it will be accepted without taking into account objections. And you are unlikely to be able to appeal it on this basis. The court may decide that you abused your right because you should have assumed that your objections would not have time to reach the inspectorate before a decision was made. see, for example, Resolution of the Federal Antimonopoly Service of the Eastern Military District dated December 25, 2013 No. A82-11448/2012; FAS UO dated September 11, 2013 No. F09-7338/13.

Similar articles

The best amulets against the evil eye and damage Amulet against the evil eye with hands for children

The best amulets against the evil eye and damage Amulet against the evil eye with hands for children

How to read the Psalter correctly

How to read the Psalter correctly

Delicious dishes with sausages

Delicious dishes with sausages

A glimpse of Bella. Romantic chronicle. A glimpse of genius. Messerer about Akhmadulina Boris Messerer glimpse of Bella romantic chronicle

A glimpse of Bella. Romantic chronicle. A glimpse of genius. Messerer about Akhmadulina Boris Messerer glimpse of Bella romantic chronicle

I dreamed that I was sailing on a boat on the river

I dreamed that I was sailing on a boat on the river

How to cook beef entrecote in a frying pan

How to cook beef entrecote in a frying pan

About the company Foreign language courses at Moscow State University

About the company Foreign language courses at Moscow State University Which city and why became the main one in Ancient Mesopotamia?

Which city and why became the main one in Ancient Mesopotamia? Why Bukhsoft Online is better than a regular accounting program!

Why Bukhsoft Online is better than a regular accounting program! Which year is a leap year and how to calculate it

Which year is a leap year and how to calculate it