Rating scale s p. Country credit rating: definition and meaning of the term

And Fitch Rating dates back to 1860. They have rated more than 100 countries with a total debt of US$34 trillion. In addition, the company is the creator of a series of S&P stock indices for the American and international securities markets. It has 6,300 employees.

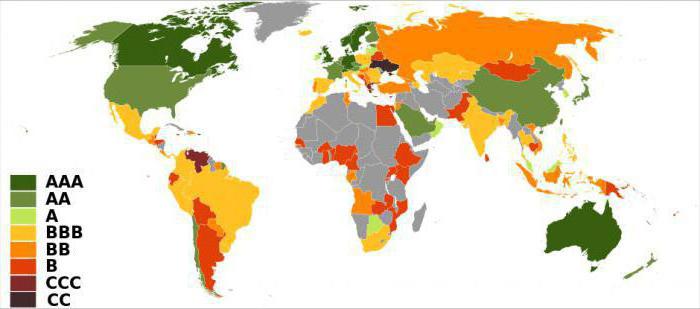

Investment grade.

“AAA” – very high ability to timely and completely fulfill one’s debt obligations; highest rating.

“AA” – high ability to timely and completely fulfill one’s debt obligations.

“A” – Moderately high ability to meet debt obligations on time and in full, with high sensitivity to the effects of adverse changes in commercial, financial and economic conditions.

"BBB" - reasonable ability to meet debt obligations on time and in full, but there is greater sensitivity to the effects of adverse changes in business, financial and economic conditions.

Speculative class.

"BB" - safe in the short term, but more sensitive to the impact of adverse changes in commercial, financial and economic conditions.

“B” – higher vulnerability in the presence of unfavorable commercial, financial and economic conditions, but currently it is possible to fulfill debt obligations on time and in full.

“CCC” – there is currently a potential for the issuer to default on its debt obligations – this is largely dependent on favorable commercial, financial and economic conditions.

“CC” – currently there is a high probability that the issuer will not fulfill its debt obligations.

“C” – bankruptcy proceedings have been initiated against the issuer or a similar action has been taken, but payments or fulfillment of debt obligations continue.

“SD” is a selective default on a given debt obligation while continuing to make timely and full payments on other debt obligations.

“D” – default on debt obligations.

- “positive” – the rating may increase;

- “negative” – the rating may decrease;

- “stable” – change is unlikely;

- “developing” – both an increase and a decrease in the rating are possible.

The S&P national rating scale uses the prefix ru: “ruAAA”, “ruAA”, “ruA” and so on. The company's rating cannot be higher than the sovereign rating. Therefore, in the description of each class it is added that the rating indicates the company's ability to pay its debt relative to other issuers.

In addition to credit ratings, S&P evaluates company management. For this purpose, the agency has developed two systems: “Corporate Governance Rating” and GAMMA – an assessment of non-financial risks associated with the purchase of shares of companies in emerging markets.

It is necessary to somehow assess the state of affairs in the state. One can impartially judge or consider a specific option for a particular case and be interested in what provides importance. For example, the probability of debt repayment. And from this point of interest is provided by the credit rating and research to establish it.

What is a credit score and research?

Credit ratings refer to the opinions of individual foreign and Russian rating agencies on the financial stability and creditworthiness of the financial sector of individual countries within their borders and internationally. To determine what value should be assigned, special studies are carried out, the purpose of which is to find out the economic situation within the country, estimate the amount of debts being paid and the likelihood of their payment if they are issued at the time of the study. Creditworthiness is a parameter that assesses the likelihood of repaying debts if you give a loan right now. Moreover, it is worth saying that ratings are practiced not only in relation to individual states, but also to large companies. Therefore, creditworthiness is a concept that applies not only to individual countries, but also to private companies.

Who is exhibiting it?

They are compiled and issued by individual rating agencies that monitor the situation in the country. They can observe either through the media and government statistics, or by combining them with reports from their representatives. For example, some bureaus interact with a number of users of different companies (through surveys), while others try to limit themselves exclusively to the largest organizations.

Why are they necessary?

Why are these ratings necessary? The fact is that they provide information to potential investors about the internal state and state of affairs. Based on their opinion, many businessmen and companies decide whether to invest their funds in a given state or organization.

Credit rating system

What credit rating systems exist? There are quite a few of them and they are designated in Latin. In general, there is a fairly wide variety of rating scales that use small letters, pros and cons, but within the framework of the article only the main “backbone” will be considered:

- AAA rating. Maximum level. This country is assumed to be the borrower with the highest level of creditworthiness. The financial situation is assessed as good and stable for a long time. The state fulfills its responsibilities on time and is extremely dependent on external factors of anthropogenic origin. Possible risks are minimal, the probability of default is close to zero.

- AA rating. Very high level of creditworthiness. This category includes states that have had a stable economic condition for a long time. Such countries are also weakly dependent on negative changes in the global economy and have a low level of credit risks.

- Rating A. High level of creditworthiness. The economic condition of states in this category is assessed as good at this point in time. All obligations are fulfilled on time. At the same time, countries have a low dependence on negative changes that occur in the global economy. The level of credit risks is assessed as low.

- BBB rating. Relatively high level of creditworthiness. This rating indicates that the economic situation of the country is quite good. It can fulfill its obligations in a timely manner and in full. At the same time, the state is moderately dependent on negative changes in the world market. The likelihood of credit risk occurring is moderate.

- BB rating. Satisfactory level of creditworthiness. These letters in the ranking indicate states whose economic situation can be assessed as acceptable. They fulfill their obligations in full and in a timely manner and are moderately affected by negative changes in the global economic market, but with negative changes in the global economy, delays are possible. are assessed as acceptable.

- Rating B. Low level of creditworthiness. The economic situation of this category of states is characterized as unstable, and the possibility of timely repayment of debts largely depends on the international situation. Credit risks in such countries are above average.

- CCC rating. Low level of creditworthiness. This includes states with an unsatisfactory economic situation. Their ability to meet their obligations is highly dependent on changes in the macroeconomic environment. The level of credit risks is considered high. There is also a significant likelihood that obligations will not be fulfilled in full or on time.

- Rating SS. Very low level of creditworthiness. The financial condition of countries included in this category is unsatisfactory. Their ability to fulfill their obligations is largely determined by changes in the external economic environment, and credit risks are very high. The probability of default is very high.

- Rating C. Unsatisfactory level of creditworthiness. The economies of countries in this category are in extremely poor condition and have extremely high risks. As a rule, countries that are in a pre-default state are included here.

- Rating D. Default. This includes countries that cannot service their obligations and, most likely, bankruptcy proceedings will be launched there. It is necessary to distinguish between these two indicators, because a default is simply a refusal to pay one’s debts; theoretically, it can be declared by the state, which can pay everything.

Let's say a word about Russia

Since each agency has its own rating scale, there are no identical opinions. But in general, Russia's rating is BBB or BB. Not the best option, but not the most hopeless either. So, the BBB rating indicates the presence of certain problems. But even among experts there is no unity. Thus, Russia’s rating is now at such a level that it can be increased if the country focuses on the development of science and the introduction of new technologies. And then the BBB rating will be raised to A. If this is not done, then a gradual decline awaits us.

Conclusion

As you can see, such seemingly simple letters can tell a lot. Behind them is the work of many people who collect and analyze the necessary information. And let's hope that the BBB rating assigned to Russia by many agencies at the moment will change to a better one.

Standard & Poor's. Long-term ratings assess the issuer's ability to timely fulfill its debt obligations. The company's ratings are graded by letter, ranging from AAA, which is assigned to exceptionally reliable issuers, to D, which is assigned to an issuer that has defaulted. Between AA and B grades there may be intermediate grades indicated by plus and minus signs (for example, BBB+, BBB and BBB-).

- AAA - the issuer has exceptionally high capabilities to pay interest on debt obligations and the debts themselves.

- AA - the issuer has a very high ability to pay interest on debt obligations and the debts themselves.

- A - the issuer's ability to pay interest and debts is highly assessed, but depends on the economic situation.

- BBB - the solvency of the issuer is considered satisfactory.

- BB - the issuer is solvent, but unfavorable economic conditions may negatively affect the ability to pay.

- B - the issuer is solvent, but unfavorable economic conditions are likely to negatively affect its ability and willingness to make debt payments.

- CCC - the issuer is experiencing difficulties with payments on debt obligations and its capabilities depend on favorable economic conditions.

- CC - the issuer is experiencing serious difficulties with payments on debt obligations.

- C - the issuer is experiencing serious difficulties with payments on debt obligations; bankruptcy proceedings may have been initiated, but payments on debt obligations are still being made.

- SD - the issuer refused to pay on some obligations.

- D - a default has been declared and S&P believes that the issuer will refuse to pay most or all of its obligations.

- NR - no rating assigned.

Short-term ratings assess the likelihood of timely repayment of short-term debt obligations. Standard & Poor's credit ratings for short-term debt are given an alphanumeric designation, ranging from the highest grade of A-1 to the lowest grade of D. Stronger obligations in the A-1 category may be marked with a plus sign. Grades from category B can also be specified with a number (B-1, B-2, B-3).

- A-1 - the issuer has an exceptionally high ability to repay this debt obligation.

- A-2 - the issuer has a high ability to repay this debt obligation, but these abilities are more sensitive to unfavorable economic conditions.

- A-3 - Adverse economic conditions are likely to impair the issuer's ability to repay the debt obligation.

- B - the debt obligation is speculative in nature. The issuer has the ability to repay it, but these opportunities are very sensitive to unfavorable economic conditions.

- C - the issuer's ability to repay this debt obligation is limited and depends on the presence of favorable economic conditions.

- D - this short-term debt obligation was declared in default.

- AAA - Highest level of creditworthiness

- AA - Very high level of creditworthiness

- A - High level of creditworthiness

- BBB - Sufficient Creditworthiness

- BB - The level of creditworthiness is below sufficient

- B - Significantly insufficient level of creditworthiness

- CCC - Possible default

- CC - High probability of default

- C - Default is inevitable

- D - Default

Moody's long-term debt ratings are opinions of the relative credit risk of fixed income debt obligations with original maturities of one year or more. They reflect the possibility that a financial obligation will not be fulfilled as promised. Such ratings are assigned on Moody's global (international) scale and reflect the likelihood of default and any financial loss in the event of default.

| Rating | Meaning |

|---|---|

| Aaa | Debt obligations rated Aaa are considered to be of the highest quality with minimal credit risk. |

| Aa | Debt obligations rated Aa are considered high quality obligations with very low credit risk. |

| A | Debt obligations rated A are considered to be in the upper mid-tier category and are subject to low credit risk. |

| Baa | Debt obligations rated Baa are subject to moderate credit risk. They are considered mid-tier liabilities and, as such, may have certain speculative characteristics. |

| Ba | Debt obligations rated Ba are considered to have speculative characteristics and are subject to significant credit risk. |

| B | Debt obligations rated B are considered speculative and subject to high credit risk. |

| Caa | Debt obligations rated Caa are considered to be of very low quality and are subject to very high credit risk. |

| Ca | Debt obligations rated Ca are highly speculative and are likely to be in default or near default. In this case, there is some probability of payment of the principal amount of the debt and interest on it. |

| C | C-rated debt is the lowest rated class of bonds and is typically in default. However, the probability of payment of principal and interest on such bonds is low. |

Note. For each overall rating category - from Aa to Caa inclusive - Moody's adds numerical modifiers 1, 2 and 3. Modifier 1 indicates that the obligation is at the top of its overall rating category; modifier 2 indicates a position in the middle of the range, modifier 3 indicates that the obligation is at the lower end of this overall rating category.

Credit rating represents an independent and reliable assessment of an issuer's creditworthiness, on the basis of which market participants can make informed financial decisions. This may entail a reduction in the issuer's costs of raising borrowed funds. For those issuers that raise funds against third-party guarantees, a credit rating may reduce the cost of such a guarantee or raise funds more efficiently without purchasing a guarantee.

In recent decades, credit ratings have become a generally accepted and convenient guide for determining the degree of creditworthiness of federal governments, regional administrations, banks, and non-financial companies. An objective assessment of the solvency of economic entities by independent experts is in modern business practice the same necessary element of doing business and public administration as regular audits.

Credit ratings are often used by banks and other financial intermediaries to make decisions on lending, money market transactions, insurance, leasing, and any other situation where an assessment of the creditworthiness of a business partner is required. Many companies choose not to disclose their financial information during business negotiations. In this case, the issuer's credit rating serves as a reliable guide to creditworthiness.

Credit rating- one of the most important tools for increasing the attractiveness of borrowers in the eyes of lenders, allowing them to obtain an objective and understandable indicator of the financial condition of borrowers. The independence of the rating agency from financial market participants contributes to increasing confidence in the borrower.

A credit score facilitates the underwriting process. Investment banks and other financial intermediaries active in the bond market may use credit ratings when planning and placing bond issues.

Principles for providing rating services

Independence: A credit rating is a rating company's independent opinion of the issuer's creditworthiness. The independence of Standard & Poor’s opinion from the interests of any market participants, government and commercial organizations is one of the most important guarantees of the objectivity and impartiality of creditworthiness assessments. Along with the high quality of analytics, independence determines the accuracy of Standard & Poor’s credit ratings.

Publicity of analytical criteria: a critical practice that provides investors with a comprehensive understanding of Standard & Poor's analytical approaches to risk assessment. All Standard & Poor’s criteria are available in various languages, including Russian, and are posted on the Standard & Poor’s website.

Collegiality: a decision-making procedure that eliminates any possibility of manipulating the opinions of analysts responsible for analyzing a particular issuer. The rating committee is the most important mechanism in the process of assigning a credit rating, guaranteeing the impartiality of analysts' assessments, quality control and the futility of putting pressure on analysts' opinions from outside. The rating committee is formed from specialized specialists depending on the industry and other features 5-9 of the issuer. The task of the rating committee includes a detailed discussion of the rating report for a given issuer and assignment of a rating at a certain level through voting.

Interactivity: the principle on which interaction with the issuer is based in the process of assigning a credit rating and subsequent monitoring of it. Based primarily on information received from the issuer itself, a painstaking, detailed discussion of all possible situations that could affect its creditworthiness. Interactivity implies regular meetings with the issuer's management and constant information contact, allowing you to quickly respond to changes.

Confidentiality of information: a fundamental operating condition that allows the issuer to guarantee non-disclosure of confidential information transferred to analysts and the publication of the rating only with the consent of the issuer.

Using rating scales: The scale allows you to compare issuers of different economic natures (corporations, regions, municipalities, banks, insurance companies, etc.) by the amount of credit risk, taking the issuer and its obligations beyond the narrow industry context.

Ongoing research into the probability of default: are carried out on the basis of a wide statistical sample across all rating categories to control the quality of the rating opinion and (if necessary) adjust the methodology.

Rating agencies

Moody's Interfax Rating Agency

Moody's Interfax Rating Agency is a universal rating agency that provides a full range of rating services for all sectors of the economy.

Aaa.ru- issuers, or debt obligations rated Aaa.ru, are characterized by the highest creditworthiness in relation to other issuers in the country.

Aa.ru- issuers, or debt obligations rated Aa.ru, are characterized by very high creditworthiness in relation to other issuers in the country.

A.ru- issuers, or debt obligations rated A.ru, have a level of creditworthiness above average among other issuers in the country.

Baa.ru- issuers, or debt obligations rated Baa.ru, represent the average level of creditworthiness among issuers in the country.

Ba.ru- issuers, or debt obligations rated by Ba.ru, have a level of creditworthiness below the average for issuers in the country.

B.ru- issuers or debt obligations rated B.ru have low creditworthiness relative to other issuers in the country.

Caa.ru- issuers, or debt obligations rated by Caa.ru, are characterized as speculative and have very low creditworthiness relative to other issuers in the country.

Ca.ru- issuers, or debt obligations rated by Ca.ru, are characterized as highly speculative and have extremely low creditworthiness relative to other issuers in the country.

C.ru- issuers, or debt obligations rated C.ru, are characterized as highly speculative and have the lowest creditworthiness relative to other issuers in the country.

Moody's Interfax Rating Agency supplements the ratings of each category from Aa to Caa indexes 1, 2 and 3. Index 1 indicates that the obligation has a higher rank in its rating category; index 2 indicates average rank and index 3 indicates lower rank in that category.

Standard & Poor's

Issuer's credit rating according to the international scale Standard & Poor's expresses a current opinion about the overall creditworthiness of the debt issuer, guarantor or guarantor, business partner, its ability and intention to timely and fully fulfill its debt obligations.

The credit rating of debt obligations on the Standard & Poor’s international scale expresses the current opinion on the credit risk of specific debt obligations (bonds, bank loans, loans, and other financial instruments).

Credit ratings on the Standard & Poor’s international scale include a long-term rating, which assesses the issuer’s ability to timely fulfill its debt obligations. Long-term ratings range from the highest, AAA, to the lowest, D. Ratings in the range from “AA” to “CCC” can be supplemented with a “plus” (+) or “minus” (-) sign, indicating intermediate rating categories in relation to the main categories.

A short-term rating is an assessment of the likelihood of timely repayment of obligations considered short-term in the relevant markets. Short-term ratings also range from 'A-1' for the highest quality obligations to 'D' for the lowest quality obligations. Ratings within the A-1 category may contain a plus sign (+) to highlight stronger obligations within that category.

In addition to long-term ratings, Standard & Poor's has specific ratings for preferred stocks, money market funds, mutual bond funds, insurance company solvency, and derivatives companies.

AAA— very high ability to timely and completely fulfill your debt obligations; highest rating.

AA— high ability to timely and completely fulfill your debt obligations.

A- moderately high ability to timely and fully fulfill its debt obligations, but greater sensitivity to the impact of adverse changes in commercial, financial and economic conditions.

BBB- sufficient ability to timely and fully fulfill its debt obligations, but higher sensitivity to the impact of adverse changes in commercial, financial and economic conditions.

BB- not at risk in the short term, but greater sensitivity to the effects of adverse changes in commercial, financial and economic conditions.

B- higher vulnerability in the presence of unfavorable commercial, financial and economic conditions, but currently it is possible to fulfill debt obligations on time and in full.

CCC— at the moment there is a potential possibility of the issuer failing to fulfill its debt obligations; Timely fulfillment of debt obligations is largely dependent on favorable commercial, financial and economic conditions.

CC— there is currently a high probability that the issuer will fail to fulfill its debt obligations.

C— bankruptcy proceedings have been initiated against the issuer or a similar action has been taken, but payments or fulfillment of debt obligations continue.

SD— selective default on a given debt obligation while continuing timely and full payments on other debt obligations.

D- default on debt obligations.

Stable - change is unlikely.

Developing - possible increase or decrease in rating.

You can also determine the credit rating of the issuer according to the Russian Standard & Poor's scale. Russian issuers mean all issuers of debt obligations, guarantors and guarantors, insurance companies located on the territory of the Russian Federation or operating on Russian financial markets. The business partner rating is a type of credit rating issuer.

An issuer's credit rating is not equivalent to the rating of its specific debt obligations, since it does not take into account the nature and collateral of the specific obligation, as well as its relative status in the event of bankruptcy or liquidation of the issuer and the protection of the rights of creditors thereunder. The creditworthiness of guarantors, or guarantors, for specific obligations of the issuer, as well as other forms of credit risk mitigation, may serve as the basis for increasing the credit rating of the obligation compared to the credit rating of the issuer.

The issuer's credit rating is not a recommendation as to whether to sell or buy the issuer's debt obligations, nor is it an opinion on the market price of debt obligations or the investment attractiveness of the issuer for a particular investor. A credit rating is based on current information obtained from the issuer or from other sources Standard & Poor's considers to be reliable. Standard & Poor's does not perform an audit in connection with any credit rating and may sometimes rely on unaudited financial information. An issuer's credit rating may be changed, suspended or withdrawn as a result of any changes in information or lack of such information or for other reasons.

Issuer credit rating:

ruAAA. The “ruAAA” issuer rating means the issuer’s very high ability to timely and fully fulfill its debt obligations relative to other Russian issuers. This is the highest credit rating on the Russian Standard & Poor's scale.

ruA. An issuer rated 'ruA' is more susceptible to adverse changes in commercial, financial and economic conditions than issuers rated 'ruAAA' and 'ruAA'. Nevertheless, the issuer is characterized by a moderately high ability to timely and fully fulfill its debt obligations relative to other Russian issuers.

ruBBB. The “ruBBB” issuer rating reflects the issuer’s sufficient ability to timely and fully fulfill its debt obligations relative to other Russian issuers. However, this issuer has a higher sensitivity to the impact of adverse changes in business, financial and economic conditions than issuers with higher ratings.

ruBB, ruB, ruCCC, ruCC. Issuers with ratings of “ruBB”, “ruB”, “ruCCC” and “ruCC” on the Russian Standard & Poor's scale are characterized by high credit risk relative to other Russian issuers. Despite the fact that such issuers have a certain degree of reliability, they are more are subject to uncertainty and the influence of unfavorable factors compared to other Russian issuers.

ruBB. An issuer with a 'ruBB' rating is characterized by lower credit risk than Russian issuers with lower ratings. However, uncertainty or the impact of adverse changes in business, financial and economic conditions may result in the issuer's insufficient ability to meet its debt obligations in a timely and complete manner.

ruB. The 'ruB' issuer rating reflects lower creditworthiness compared to the 'ruBB' rating. Currently, this issuer is able to fulfill its debt obligations on time and in full. However, adverse changes in commercial, financial and economic conditions are likely to prevent the issuer from meeting its debt obligations on time and in full.

ruCCC. The issuer rating of “ruCCC” means that at the moment, in the conditions of the Russian financial market, there is a potential possibility of default on its debt obligations. Timely fulfillment of debt obligations is largely dependent on favorable commercial, financial and economic conditions.

ruC. The issuer rating “ruС” is assigned when bankruptcy proceedings have been initiated against the issuer, a ban on carrying out its core activities has been imposed, a court decision on the imposition of foreclosure on property is expected, or in another similar case. During the trial (or external management), the relevant authority may decide to repay part of the debt obligations and default on the remaining obligations. Standard & Poor's debt rating description provides more detailed explanation of the possible impact of such decisions on the credit rating of specific debt obligations.

Rating "ruSD" in the conditions of the Russian financial market, assigned when Standard & Poor's believes that the issuer has defaulted on a specific issue or several issues of its debt obligations, but will continue to make timely and full payments on other debt obligations. In the description of the credit rating of debt obligations Standard & Poor "s provides a more detailed explanation of the possible impact of these types of decisions on the credit rating of specific debt obligations.

Standard & Poor's specialized ratings assign certain types of debt obligations, bank loans, investment projects and private placements of securities, using the same scale as for other debt instruments. Private placement ratings include an assessment of the guarantees and collateral required to reduce the risk of loss in the event of default. Bank loan ratings serve the needs of the syndicated loan and project finance markets and include an assessment of the lender's prospects for obtaining funds in the event of default, which is based on an analysis of the value of collateral or other protective mechanisms typically provided in such schemes. .

Bank loans, private placements and other financial instruments, such as guaranteed bonds, may receive a higher rating than the issuer's rating when they are well protected and adequately compensate the lender. In contrast, instruments that are inferior in repayment priority to the issuer's principal generally have a lower rating than the issuer's rating.

Many mutual fund managers use Standard & Poor's ratings for the funds they manage to highlight the strengths of their bond and cash funds relative to their competitors. The ratings provide investors with information about the funds' creditworthiness and the quality of their management.

Credit ratings of structured instruments include assessment of:- the quality of the assets being securitized;

- payment structures;

- legal purity of transactions.

The use of structured instruments makes it possible to reduce credit risks by removing securitized assets from the issuer’s balance sheet.

The priority of tranches when issuing structured instruments allows obligations to be issued with a credit quality higher than the credit quality of the securitized assets.

Stock market indicators are Standard & Poor's indices, used by investors around the world to evaluate investment performance and as a basis for a wide range of financial instruments, such as index funds, deposit products, futures, options and exchange-traded funds ( ETFs). The S&P 500 index includes 500 companies - leaders of the leading sectors of the American economy and covers more than 80% of the shares of American companies. The S&P Global 1200 Index covers approximately 70% of the world's capital markets and includes the seven most widely used indices, many of which are leaders in their regions. Standard & Poor's indices are created as investment portfolio indices that are broadly representative of the market while still having practical relevance to investors.

Fitch Ratings

Ratings Fitch Ratings represent opinions regarding the ability of issuers to timely meet their financial obligations or the timely repayment of securities issues, including obligations such as interest payments, preferred stock dividends or payments of principal. Ratings may be assigned to a wide range of issuers and securities, including sovereigns, governments, structured finance instruments and corporate issuers; debt obligations, preferred shares, bank loans and counterparties. Ratings can also assess the financial strength of insurance companies and financial guarantors.

Credit ratings are used by investors as indicators of the likelihood that payments will be made in accordance with the terms under which the investment was made. Thus, the use of credit ratings determines their function: investment grade ratings (international long-term "AAA" - "BBB"; short-term "F1" - "F3") denote a relatively low probability of default, while speculative, or non-investment grade, ratings ( Sub-investment category (international long-term "BB" - "D"; short-term "B" - "D") may indicate a higher probability of default or that a default has already occurred.

The ratings are not predictive of the likelihood of default, but it should be noted that over the long term, the default rate for US corporate bonds rated 'AAA' has averaged less than 0.10% per year, while the default rate for bonds rated "BBB" reached 0.35%, and bonds rated "B" - 3.0%.

Issuers or issues of securities rated at the same level have similar, but not necessarily identical, creditworthiness because the rating categories do not fully reflect subtle differences in credit risk.

Fitch Ratings' credit ratings and research are not recommendations to buy, sell, or hold any security. Ratings do not constitute commentary on the adequacy of market price, the suitability of any security for any particular investor, or the application of tax exemptions or tax treatment to any payments made in respect to any security.

The ratings are based on information obtained directly from issuers, other obligors, underwriters, their experts and other sources Fitch believes to be reliable. Fitch does not audit or verify the accuracy or accuracy of such information. Ratings may be changed or withdrawn as a result of changes or unavailability of information or other reasons.

Ratings assigned to equity programs relate only to standard issues within a particular program. These ratings do not apply to all releases within the program. In particular, for non-standard issues, i.e. those related to third party loans or index performance, their ratings may differ from the rating of the corresponding program.

Credit ratings do not directly assess any risks, with the exception of credit risks. In particular, these ratings do not address the risk of loss due to changes in interest rates or other market factors.

Individual ratings assigned only to banks. The purpose of these internationally comparable ratings is to evaluate the bank if it were completely independent and could not rely on external support. These ratings assess a bank's risk exposure, risk appetite and risk management and thus represent the agency's view of the likelihood of the bank encountering significant difficulties such that the bank would require support.

The main factors that the agency analyzes when assessing a bank and determining the level of this rating include profitability and balance sheet integrity (including capitalization), customer base and management, operating environment and development prospects. Finally, an important factor is the consistency of policies and the size of the bank (volume of own funds) and diversification (scale of activity in different sectors of the economy and geographical coverage).

An exceptionally stable bank. Characteristics of such a bank may include exceptionally high profitability and balance sheet integrity, a very large customer base and high quality management, and an exceptionally favorable operating environment and development prospects.

A stable bank with no significant concerns. Characteristics of such a bank may include high profitability and balance sheet integrity, a large customer base and high quality management, a favorable operating environment and development prospects.

A bank with adequate strength, but at the same time characterized by one or more factors that cause concern. There may be concerns about the profitability and balance sheet integrity of such a bank, the size of its customer base and quality of management, operating environment or development prospects.

A bank that is characterized by certain shortcomings, both internal and associated with external factors. There are concerns about its profitability and balance sheet integrity, customer base and quality of management, operating environment or growth prospects. Banks operating in emerging economies inevitably face a greater number of potential weaknesses due to external factors.

A bank experiencing very serious difficulties and which already requires, or is likely to require, external support.

Economic growth and recovery will continue, but will be slow, says S&P. They will be supported by a rebound in oil prices, a moderate expansion of domestic demand, as well as an improvement in the situation in the global economy. Problems with private banks have not undermined financial stability, the agency notes. It also sees signs of a recovery in lending. At the same time, demographic challenges and low productivity will continue to constrain long-term growth. The agency expects the government to launch reforms to boost productivity, stimulate investment and ease pressure on the economy from an aging population and a shrinking workforce. But these initiatives are not aimed at overcoming key structural obstacles. Despite the movement towards reforms after the presidential elections, government policy will be more likely to focus on ensuring macroeconomic stability and creating budget buffers, S&P notes.

The Agency cautiously assesses the prospects for a significant improvement in the business environment in Russia, including the judicial system. S&P does not expect a significant reduction in the role of the state in the economy. Russia suffers because of a weak system of checks and balances between institutions and power; institutions are weak. This is reflected in recent actions restricting independent media.

S&P may lower its rating for the worse if foreign countries significantly tighten sanctions against Russia, the agency notes. Another reason could be a worsening budget situation, the report notes.

How they reacted in Russia

Raising the sovereign rating to investment level is a belated reaction to the successes of Russian economic policy, Russian Minister of Economic Development Maxim Oreshkin commented on S&P’s decision. According to him, the decision is primarily due to the implementation of a responsible macroeconomic policy.

“The floating exchange rate, inflation targeting, and the new design of the fiscal rule contributed to a significant reduction in the dependence of the Russian economy on the oil price environment,” Oreshkin said in his commentary. Raising Russia's rating to investment grade will facilitate the influx of capital and ensure that the yield level on the OFZ market remains below 7% for long-term securities, the minister added.

Russian Finance Minister Anton Siluanov called the rating agency's decision logical and expected. “Our economy has adapted very quickly to new conditions and is showing positive growth rates,” the minister’s comment says. He noted that Russia today is experiencing record low inflation, a stable ruble exchange rate, and stable budget execution. The revision of the sovereign rating will have a positive impact on a similar increase in the ratings of corporate market participants and banks, Siluanov noted.

The presence of investment ratings from two agencies will mean the inclusion of Russian securities in the global indices of JPMorgan and Barclays, which the funds are guided by, as stated earlier by the director of the analytical department of Loko-invest, Kirill Tremasov. Accordingly, an influx of money that can be estimated at a couple of billion dollars, he pointed out.

There is no point in expecting a mechanical acceleration of capital inflows into the domestic market after the S&P rating upgrade, because the ratings in the local currency were already at investment level, the chief economist believes “ VTB capital" in Russia Alexander Isakov. At the same time, the rating upgrade is good news for sovereign Eurobond prices: it will allow Russia to return to indices such as Barclays Global Aggregate and EMBI IG, which should encourage the influx of conservative funds. VTB Capital also expects a corresponding increase in the rating of quasi-sovereign borrowers.

The Ministry of Economic Development is waiting for Moody's

After the S&P rating upgrade, Moody's remains the only international agency from the Big Three that maintains the Russian rating at a speculative level. Previously, it was the last raised the outlook for Russia's sovereign rating from "stable" to "positive". This happened at the end of January. Then Moody's that the rating can be increased if experts make sure that the vulnerability of the Russian economy to external risks is reduced. Otherwise, a downgrade in forecasts is not excluded, the rating agency warned. Among the risks experts Moody's named the possibility of reducing the lending capacity of banks in the event of the introduction of additional sanctions and even further restriction of access to international capital markets.

S&P downgraded Russia's creditworthiness to speculative level in January 2015. This was preceded by the introduction of US and EU sanctions, a collapse in oil prices and a sharp depreciation of the ruble. Following S&P in 2015, Moody's also lowered Russia's rating to speculative. At the investment level, only Fitch retained the Russian rating. On Friday, it did not raise the Russian rating, leaving it also at the “BBB-” level.

Over the past year, all three agencies have raised their rating forecasts for Russia to a “positive” level. S&P did this last March, Fitch- in September, Moody's - at the end of January this year. The Ministry of Economic Development expects Russia's rating to be increased by all international rating agencies in 2018, said Minister Maxim Oreshkin in an interview with the Rossiya 24 TV channel at the end of January. According to him, the agencies "“overdid it” when they lowered their grades, and now “they are trying to delay the moment of increase as much as possible in order to minimally admit the mistakes they made.”

“All economic indicators, especially considering that the economy has returned to growth, and low inflation, and the budget is now entering the surplus zone, and we are again starting to accumulate money in sovereign funds,–they are saying that the rating should be not just in the investment category, but even several positions higher,”–noted Oreshkin.

Related articles

The best amulets against the evil eye and damage Amulet against the evil eye with hands for children

The best amulets against the evil eye and damage Amulet against the evil eye with hands for children

How to read the Psalter correctly

How to read the Psalter correctly

Delicious dishes with sausages

Delicious dishes with sausages

A glimpse of Bella. Romantic chronicle. A glimpse of genius. Messerer about Akhmadulina Boris Messerer glimpse of Bella romantic chronicle

A glimpse of Bella. Romantic chronicle. A glimpse of genius. Messerer about Akhmadulina Boris Messerer glimpse of Bella romantic chronicle

I dreamed that I was sailing on a boat on the river

I dreamed that I was sailing on a boat on the river

How to cook beef entrecote in a frying pan

How to cook beef entrecote in a frying pan

About the company Foreign language courses at Moscow State University

About the company Foreign language courses at Moscow State University Which city and why became the main one in Ancient Mesopotamia?

Which city and why became the main one in Ancient Mesopotamia? Why Bukhsoft Online is better than a regular accounting program!

Why Bukhsoft Online is better than a regular accounting program! Which year is a leap year and how to calculate it

Which year is a leap year and how to calculate it