Planned advance in 1s 8.3. “1C Enterprise Accounting” edition “3.0”: setting up advance payment and parsing the new document “Writ of Execution”

For example, it is necessary for the first half of January 2016. From our example, the advance is paid according to the calculation for the first part of the month. To do this, you need to create a document “Accruals for the first half of the month.” By default, in 1C ZUP 3.0 this document is available in the “All Accruals” journal.

In the form “Accruals for the first half of the month” we indicate the month, organization and calculation for the first half of the month until 01/15/2016. That is, the calculation is made from 01/01/2016 to 01/15/2016. Next, click the “Fill” button, which will analyze all the planned accruals of employees and calculate the result taking into account the standard time for the entire month and the time worked for the first part of the month, from 01/01/2016 to 01/15/2016:

1C 8.3 ZUP 3.0 generates all planned accruals for employees, for which the settings indicate that they are accrued when calculated in the first half of the month:

Planned accruals may include:

- Salaries, allowances.

- For employees who work at night according to a work schedule or according to a time sheet, 1C ZUP 3.0 automatically calculates an additional payment for going to work at night.

- If an employee is assigned a shift schedule and the working hours on this schedule coincide with a holiday, then an additional payment is automatically added for going to work on holidays.

- Work on holidays, weekends and overtime registered up to this point are also credited to the advance payment.

- Planned employee retentions are also included in the advance. For example, if a writ of execution is registered for an employee. And so on.

It should be noted that in 1C 8.3 ZUP 3.0, the accrual document for the first half of the month makes a certain calculation, which in the future will be used only when paying the advance. Everything that is accrued is conditionally accrued, and what is calculated is the results of a preliminary calculation in order to pay a certain amount in advance. These amounts do not appear in the accrual register; this is simply a preliminary calculation.

Also in the accrual document for the first half of the month, personal income tax is calculated. But this is not a tax charge, it is just a preliminary calculation:

The result of this calculation (everything that is accrued minus everything that is withheld) is recorded in the register as the amount of the advance payment. If, after making an advance, you try to create a summary or payroll, there will be no numbers there. Because this is not an accrual, this is a preliminary calculation.

What will happen if you do not generate the document “accrual of advance payment for the first half of the month” in 1C ZUP 3.0 (8.3)?

The advance payment can be calculated using different accrual methods, and if there are settings for the calculation, then this document must be generated. If you do not enter it, then nothing will be included in the advance payment when filling out the statement. If the advance is calculated as a fixed amount or as a percentage of the payroll, then in 1C ZUP 3.0, when filling out the payment form, employees with the advance amounts will automatically be included.

How to pay an advance in 1C ZUP 3.0 (8.3)

Having made a preliminary calculation in 1C ZUP 3.0, you can pay an advance. In the “all statements” section, we create a corresponding payment statement, the purpose of which indicates the payment of an advance.

Select the “Payments” menu, then “all statements” - statement to the cashier. In the document we indicate “pay an advance”, select the month of payment, January, the date of payment of the advance and click the “fill out” button. 1C ZUP 3.0 automatically generates everything that is accrued in the advance:

If we talk about working in conjunction with 1C ZUP 3.0 and 1C 8.3 Accounting, then first in 1C ZUP 3.0 a statement for payment is drawn up, synchronized with 1C 8.3 Accounting, where the payment is reflected. You can reflect the payment in 1C 8.3 Accounting to a current account or to the personal accounts of employees, or through the cash register. After you have reflected the transfer of personal income tax in 1C 8.3 Accounting, in 1C ZUP 3.0 you must indicate the details of the payment document with which the personal income tax is transferred and conduct the statement.

Withholding personal income tax when paying an advance in 1C ZUP 3.0 (8.3)

Personal income tax is not withheld or transferred from the advance, but if the advance includes the payment of other income, for example, financial assistance or temporary disability benefits, on which tax must be withheld, then personal income tax is withheld and must be paid.

In 1C ZUP 3.0, those payments that need to be paid along with the advance are automatically added to the advance payment. For example, when paying financial assistance in advance, income tax is withheld. This tax must be transferred:

Let us remind you that income tax is paid no later than the day following the day of payment for all income, except for temporary disability benefits and vacation payments. For vacation pay and sick leave benefits from 2016, the deadline for paying personal income tax is until the end of the month in which the income was received. For all other income, including wages, financial assistance, the deadline for transferring personal income tax is the next day after the day of payment.

Please rate this article:

The developers of accounting software, with the goal of helping users make automatic payroll accounting, made an important contribution. In particular, new documents called “Vacation” and “Sick Leave” were created in 1C.

Now, using the program, the accountant has the opportunity to accrue not only disability benefits and vacation, but also in the case of calculating accruals (depending on the time worked), make a transfer, taking into account days missed due to vacation or illness.

In today's material we will focus your attention on 2 innovations in payroll accounting. One of them is a document named “Writ of Execution”, the other is the ability to automate the payment of an advance.

In this case, you can choose one of 2 types: a percentage of the tariff or a fixed amount. We will tell you more about all this in today's material.

How can I make it possible to use writs of execution in “Accounting Settings”?

First, let’s explain the purpose for which a document called “Writ of Execution” is used. On its basis, a certain amount is deducted from the employee’s salary for the purpose of paying alimony (money intended for the maintenance of minors). Russian legislation provides for 25 percent of earnings per child; for two - 1/3; for three - more than 50%. However, there may be a situation where the court changes the existing rules for a specific situation and sets a fixed amount of alimony.

In order for the 1C accounting program to have access to a document with the name document “Execution Sheet”, you need to set the necessary setting in the “Accounting Settings”. Namely, on the tab called “Salaries and Personnel”, enable the parameter named “Keep records of sick leave, vacations and executive documents.” It should be noted that all these documents can only be used in a database where the staff does not number 60 people.

"1C BUKH": new document "Writ of Execution"

After making the main menu tab called “Salaries and Personnel”, access to a document called “Writ of Execution” will open. It's quite simple, so you shouldn't have any questions about it. We emphasize that the recipient is selected from the “Counterparties” directory, and not from the “Individuals” directory. In addition, you can choose the payment method in two ways: a fixed amount or a percentage. The third option is to indicate a certain share of earnings: for example, 1/3. We cannot indicate this value as a percentage, so the program developers give us another opportunity - to indicate the share as a fraction.

And one more important nuance. In our example, we did not mark the end date for this content.

This means that it will continue to operate until we stop it. Although there is no special document intended to terminate detention. To carry out this operation, you need to go to the output document, and then enter the end date in it. It is the content that will be calculated automatically and displayed in a document called “Payroll”.

In this document, there is a tab of the same name for all deductions. Also, the total amount of deductions for the company’s employees can be seen on the main tab called “Employees”.

Let us remind you that deductions under writs of execution are calculated not from the total amount of accrual, but from the amount of accrual reduced by the amount of calculated personal income tax. Calculations are carried out using the following formula:

15 748,06 = (54 303,15 - 7059) * 1/3

"1C Accounting" edition "3.0": setting up advance payment

Another update in the 1C accounting program that we will tell you about is the automation of advance payment calculations. This is a good addition to the new documents called “Sick Leave”, “Vacation” and “Writ of Execution”. It is worth noting that starting from “3.0.37” you can configure the options for calculating the advance payment. Therefore, with a lower release, update “1C”. So, the setting for calculating the advance payment is contained in the form of a directory element named “Employees”. As we noted earlier, there are 2 options for an advance: a fixed amount or a percentage of the tariff. Select a specific option and then enter a specific amount or percentage.

In the accounting program “1C BUKH”, the fact of salary payment can be displayed using two documents: “Statement to the bank” or “Statement to the cashier”. You will find them on the tab of the main menu of the accounting program called “Salaries and Personnel”. An interesting nuance: even if the employee’s salary account is not indicated in the database, a document called “Statement to the Bank” will still be filled out. But that's a completely different topic. In order to set up automatic filling of advance payment amounts, in the field called “Pay”, select “Advance”, and then click “Fill”. In the example we offer, employee Sorokin receives a salary of 50,000 rubles and an advance of 40 percent of the salary. This means that he should be given 20,000 rubles in advance.

Well, if we have already touched on the topic of paying salaries through a banking institution, let us remind you that the personal account number for a specific employee must be indicated on the tab called “Payment and accounting of salaries” of the directory element form with the name “Employees”.

It is here that you also need to choose an agreement with a banking institution, that is, a salary contract. However, here you can only select it. And you can create a salary project in the directory of the same name, which is located in the section of the main menu called “Salaries and Personnel” (a group of links named “Directories and Settings”). The element of this directory contains information about the bank and the agreement with this banking institution.

If there are too many employees at a particular enterprise, then it will be too burdensome for one accountant to personally enter personal account information for each employee. For group entry of data on personal accounts in the 1C accounting program, there is a form called “Entering personal accounts.” You can find a link to this form on the main menu tab named “Salaries and Personnel” in the “Salary Projects” group.

Every accountant sooner or later encounters advance payments (whether to their suppliers or advances from buyers) and in theory knows that according to the requirements of the Tax Code of the Russian Federation (Article 154, paragraph 1; Article 167, paragraph 1, paragraph 2 ) VAT must be calculated on the advance payment on the date of its receipt. Our article today is about how to do this in practice with advance invoices in the 1C 8.3 program.

Making the initial settings

Let's take a look at the company's accounting policy and check whether the tax regime we have indicated is correct: OSNO. In the “Taxes and Reports” section in the “VAT” tab, the program gives us a choice of several options for registering advance invoices (Fig. 1) (we need this setting when we act as a seller).

We may not register advance invoices in 1C if:

- the advance was credited within five days;

- the advance was credited until the end of the month;

- the advance was credited until the end of the tax period.

It is our right to choose any of them.

Let's analyze the offset of advances issued and advances from the buyer.

Accounting in 1C for advances issued.

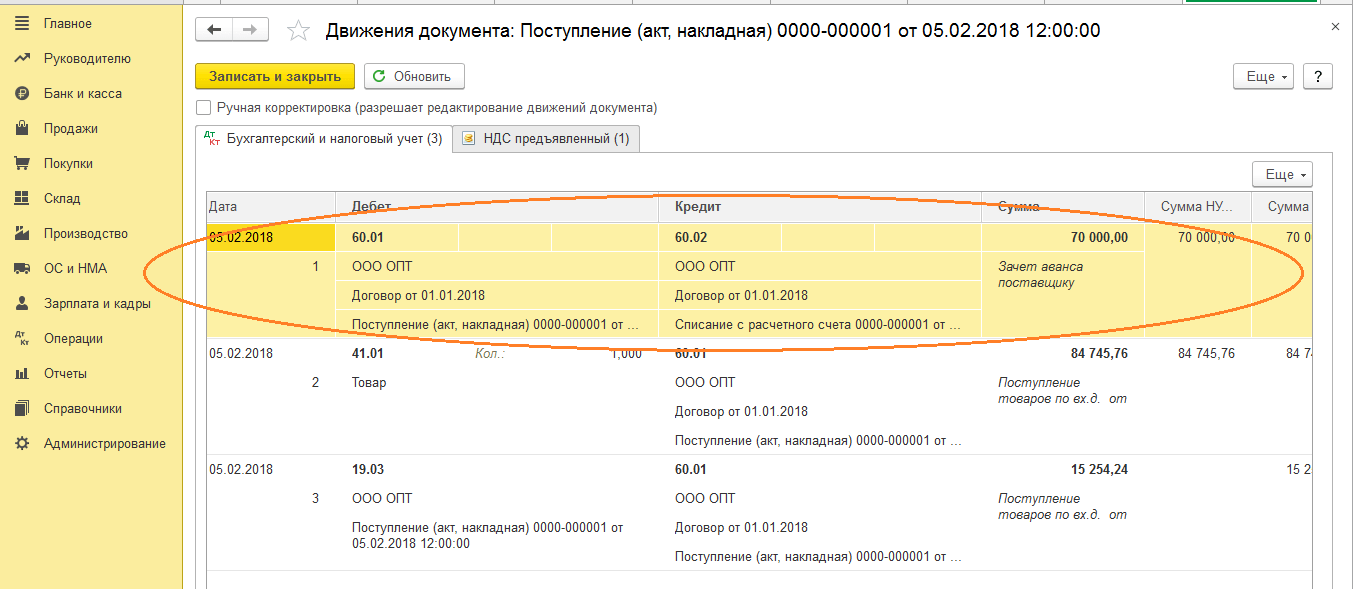

For example, let’s take the trading organization Buttercup LLC (we), which entered into an agreement with the wholesale company OPT LLC for the supply of goods. According to the terms of the contract, we pay the supplier an advance of 70%. After which we receive the goods and pay for them completely.

In BP 3.0 we draw up a bank statement “Debit from current account” (Fig. 2).

Please pay attention to important details:

- type of transaction “Payment to supplier”;

- contract (when posting goods, the contract must be identical to the bank statement);

- VAT interest rate;

- offset of the advance payment with VAT automatically (we indicate a different indicator in exceptional cases);

- When posting a document, we must receive correspondence of 51 invoices with the supplier's advance invoice, in our example it is 62.02. Otherwise, an invoice for the advance payment in 1C will not be issued.

Having received payment, OPT LLC issues us an advance invoice, which we must also post in our 1C program (Fig. 3).

On its basis, we have the right to accept the amount of VAT on the advance as a deduction.

Thanks to the “Reflect VAT deduction in the purchase book” checkbox, the invoice automatically goes into the purchase book, and when posting the document, we receive an accounting entry with the formation of invoice 76.VA. Please note that the transaction type code 02 is assigned by the program independently.

Next month OPT LLC ships the goods to us, we receive them in the program using the document “Receipt of Goods”, and register an invoice. We do not correct accounts for settlements with the counterparty; we select “Automatic” for debt repayment. When posting the “Receipt of Goods” document, we must receive a posting for the offset of the advance payment (Fig. 4).

When filling out the document “Creating sales book entries” for February, we receive automatic completion of the “VAT Restoration” tab (Fig. 5), and this amount of restored VAT ends up in the sales book for the reporting period with transaction code 22.

To reflect the final payment to the supplier, we can copy and post an existing document “Write-off from the current account”, indicating the required amount.

We create a purchase book, which reflects the amount of our VAT deduction on prepayment with code 02, and a sales book, where we see the amount of restored VAT after receiving the goods with transaction type code 21.

Accounting in 1C for advances received

For example, let’s take an organization familiar to us, LLC “Lutik” (we), which entered into an agreement with the company LLC “Atlant” for the provision of goods delivery services. According to the terms of the agreement, the buyer of Atlant LLC pays us an advance of 30%. After which we provide him with the necessary service.

The method of working in the program is the same as in the previous version.

We formalize the receipt of an advance in 1C from the buyer with the document “Receipt to the current account” (Fig. 6), followed by registration of an advance invoice, which gives us accounting entries for calculating VAT on the advance (Fig. 7).

You can register an invoice for an advance payment in 1C directly from the document “Receipt to the current account”, or you can use the processing “Registration of invoices for an advance payment”, which is located in the “Bank and cash desk” section. In any case, it immediately goes into the sales book.

At the time of the document “Sales of services”, the buyer’s advance will be credited (Fig. 8), and when the document “Creating purchase book entries” is executed (Fig. 9), the amount of VAT on the advance received will be deducted, account 76.AB is closed (Fig. .10).

To check the fruits of his work, an accountant usually only needs to create books of purchases and sales, as well as analyze the “VAT Accounting Analysis” report.

Work in 1C with pleasure!

If you still have questions about advance invoices in 1C 8.3, feel free to ask us on the dedicated line. They work 7 days a week and will help in the most difficult situations in tax and accounting.

Let's look at the operation of standard 1C functionality (in the configurations "1C: Manufacturing Enterprise Management for Ukraine", "1C: Salaries and Personnel Management for Ukraine" and "1C: Agricultural Enterprise Management for Ukraine" (from release 2.1.40 and higher).

To calculate and pay an advance in the above configurations, create a document “Accrual of salaries for employees of the organization” with the “Preliminary calculation” flag turned on with the date of payment of the advance. To automatically fill out and calculate the document, click the “Fill and calculate all” button (Fig. 1).

Fig 1. Document “Payroll for employees of organizations”

To record time worked you should:

When using the deviation method, record absenteeism, vacations, sick leave, etc. relevant documents;

When using the direct timesheet method, it is necessary to generate a “Working Time Sheet” document. The document can be filled out either for the first half of the month (strictly from the 1st to the 15th), or for an arbitrary period.

The configurations provide options for conveniently filling out this document. For example, you can fill out a document with a list of employees for whom the advance amount is calculated (the “Fill” button in the “Employees” tabular section), fill out the accruals (the “Fill” button in the document command panel or in the “Accruals” tabular section) and perform the calculation (the "Accruals" button “Calculate” in the command panel of the document or in the “Calculate” tabular section).

You can analyze the accrual process for a specific employee using the “Calculate” and “By employee with comments” buttons (Fig. 2).

Fig 2. Document “Payroll for employees of organizations” with comments

Let's look at the example of employee Lutskova L.P. The accountant calculates the advance payment for September, document dated September 15, 2015. All primary data was entered using the document “Hiring to the organization” and is stored in the information register “Planned accruals of the organization’s employees” (Fig. 3).

Fig 3. Document “Hiring to an organization”

In the comments to the document “Calculation of salaries for employees of organizations” (Fig. 2) it is clear that “Salary by day” is a type of calculation (specified upon hiring), the calculation method is “At the monthly tariff rate”, the calculation procedure is indicated in the calculation type “Calculation type plans”\”Basic accruals of organizations” (Fig. 3).

In our example, the paid time in days is calculated according to the “Five-day” work schedule (the schedule is specified upon hiring) until the document date (09.15.15) and amounted to 11 days. The time standard of 22 days is also taken from the work schedule (Fig. 4).

Figure 4. Directory “Work Schedules”

The tariff rate is indicated in the document “Hiring of organizations” and can be changed using the documents “Entering information on planned accruals of employees of organizations”, “Personnel transfer of organizations”.

The calculation result is 8500 =17000/22*11

Payment of an advance for time worked is documented in the document “Salaries payable to organizations” with the type of payment “Advance (based on preliminary calculation)” (Fig. 5).

This document calculates all taxes that should be transferred from this advance payment by clicking the “Calculate taxes” button. The “Amount” column will indicate the calculated amount to be paid.

Fig 5. Document “Salaries payable by organizations”

The program provides payment methods through a bank and through a cash register. In order to make a payment through a bank, you must fill out the document “Entering information about employees’ bank cards.”

Fig 6. Document “Entering information about employees’ bank cards”

Depending on the method of payment, on the basis of the document “Salaries payable to organizations”, a document “Outgoing payment order” (with the type of operation “Transfer of wages”) or a document “Expenditure cash order” (with the type of operation “Payment of wages according to statement”) is generated. .

Fig 7. Document “Outgoing payment order”

Fig 8. Document “Cash receipt order”

Payment documents for advance payment and tax payments can be generated automatically using processing called up by clicking the “Go” button from the “Salaries payable to organizations” document.

Fig 9. Processing “Generation of payment documents for contributions to funds”

When you click the “Create” and “Post” buttons, “Outgoing Payment Order” documents will be generated with the type of operation “Tax Transfer”.

To automatically generate payment documents for paying taxes, you must fill out the information register “Parameters of payment documents for contributions to funds.”

Fig 10. Register of information “Parameters of payment documents for contributions to funds”

The program allows you to pay advances in a fixed amount.

To do this, you need to fill out the information register “Advances to employees of organizations” and generate a document “Salaries payable” with the type of payment “Advance”.

Figure 11. Register of information “Advances to employees of organizations”

Fig 12. Document “Salary payable”, type of payment “Advance”

It should be noted that in the document “Types of payments: Advance” the flag “Calculation from the reverse” is set, so the amount “net” is entered into the information register “Advances to employees of organizations”, that is, what a person should receive “in hand”. In our example, Sergey Dmitrievich Filin will receive 2500 UAH. (Fig. 11 and 12), but the entire amount will be credited in the system (“Dirty Amount”).

Figure 13. Directory “Types of payments”

Lyudmila LUTSKOVA, 1C:Enterprise product consultant, Implementation Center [you must register to view the link], Candidate of Economic Sciences.

Based on materials: [you must register to view the link]

2016-12-08T14:03:45+00:00

- Write to register " VAT Purchases" ensures that the issued advance is included in the purchase book.

Forming a shopping book

We create a purchase book for the 1st quarter:

And here is the received invoice for the advance payment:

We look at the final VAT refund for the 1st quarter

There were no other business transactions in the 1st quarter, which means we can safely form the “VAT Accounting Analysis”:

VAT refund for the 1st quarter was 13,728 rubles 81 kopecks:

2nd quarter

Receipt of goods

We enter into the program the receipt of goods from LLC "Supplier" on 04/01/2016 in the amount of 150,000 rubles (including VAT):

Create a new document:

The invoice from the supplier will be like this:

In the invoice received from the supplier, the amount “excluding VAT” was not highlighted as a separate line. Therefore, before filling out the tabular part, we set the tax calculation method as “VAT in total”.

We analyze the postings and movements of registers...

- The previously paid advance to the supplier was credited to debit 60.01 in correspondence with credit 60.02 in the amount of 90,000 rubles.

- 127,118.64 (150,000 minus VAT) went to the cost of goods (to the debit of account 41.01) in correspondence with our debt to the supplier (credit 60.01).

- 22,881.36 went to “input” VAT, which we will accept for offset (debit 19.03) in correspondence with our debt to the supplier (credit 60.01).

- An entry (with a + sign, receipt) in this register accumulates our “incoming” VAT (similar to an entry in the debit of account 19).

Register the received invoice

Together with the invoice, Supplier LLC gave us a regular invoice dated 04/01/2016 for the amount of 150,000 rubles (including VAT).

To register it, go to the newly created document “Receipt of goods” and at the very bottom:

- We enter the number and date of the invoice from the supplier.

- Click the "Register" button

We will not analyze in detail the wiring and movements of this texture, since we have already dealt with this in part.

We look at the VAT refund for the 2nd quarter

We again form the “Analysis of VAT accounting” (this time for the 2nd quarter):

VAT refundable for the 2nd quarter was equal to 22,881.36:

Why 22,881.36?

This is VAT on a single invoice received from a supplier in the second quarter in the amount of 150,000 (including VAT): 150,000 * 18 / 118 = 22,881.36.

But what about the already accepted VAT in the amount of 13,728.81 for the 1st quarter on an advance payment of 90,000, you ask?

And you will be absolutely right.

After all, VAT on the advance payment we took as offset in the 1st quarter must be accrued (reinstated) by us for payment in the 2nd quarter, when the goods arrived and we received a regular invoice from the supplier for the full amount.

This is exactly what the entry in the gray box in the VAT analysis report indicates to us:

Making an entry in the sales book

To restore the VAT taken as offset from the advance payment, go to the “VAT Accounting Assistant”:

In the document that opens, go to the “Recovery by Advances” tab and click the “Fill” button:

The program discovered that the advance payment, from which we offset VAT in the 1st quarter, was offset (a regular invoice document for the same buyer and agreement) in the 2nd quarter.

And now his VAT needs to be restored for payment through the sales book - otherwise we would have offset the VAT on the advance twice:

We post the document “Creating sales book entries” through the “Post and close” button:

![]()

Let's analyze the transactions and register movements of the sales book entry document...

- We restore VAT from the advance issued in the 1st quarter to the debit 76.VA (VAT on advances issued) in correspondence with the credit 68.02.

Related articles

The best amulets against the evil eye and damage Amulet against the evil eye with hands for children

The best amulets against the evil eye and damage Amulet against the evil eye with hands for children

How to read the Psalter correctly

How to read the Psalter correctly

Delicious dishes with sausages

Delicious dishes with sausages

A glimpse of Bella. Romantic chronicle. A glimpse of genius. Messerer about Akhmadulina Boris Messerer glimpse of Bella romantic chronicle

A glimpse of Bella. Romantic chronicle. A glimpse of genius. Messerer about Akhmadulina Boris Messerer glimpse of Bella romantic chronicle

I dreamed that I was sailing on a boat on the river

I dreamed that I was sailing on a boat on the river

How to cook beef entrecote in a frying pan

How to cook beef entrecote in a frying pan

About the company Foreign language courses at Moscow State University

About the company Foreign language courses at Moscow State University Which city and why became the main one in Ancient Mesopotamia?

Which city and why became the main one in Ancient Mesopotamia? Why Bukhsoft Online is better than a regular accounting program!

Why Bukhsoft Online is better than a regular accounting program! Which year is a leap year and how to calculate it

Which year is a leap year and how to calculate it